View in web for best experience

Happy Monday, Industry 4.0!

Memorial Day weekend is six days away, which means a few things are about to happen in manufacturing facilities across the country: somebody's going to fire up a grill that hasn't been touched since last September, somebody's going to discover their lake house dock needs more repairs than it did last fall, and somebody is definitely going to volunteer to "keep an eye on things" remotely so they can answer one Slack message every four hours and call it a working weekend.

It's also a holiday that matters. So before we get into the news, a sincere thanks to the veterans in our audience — and to everyone who's lost someone who served.

A quick housekeeping note: next week's newsletter will go out on Tuesday, May 26th instead of Monday, since most of you (rightfully) won't be reading email on Memorial Day. Same content, same depth — just one day later.

Now, about last week. While most of us were trying to remember where we put the patio cushions, the Industry 4.0 world had one of its busiest stretches in months. In 72 hours: Foxconn admitted ransomware attackers had its Wisconsin plant filling out paper timesheets for eleven days. SAP told 30,000 people in Orlando that the future of enterprise software is software that runs the business for you. And IoT Analytics quietly published a report saying the much-celebrated "reshoring boom" is, statistically speaking, not actually happening.

Three stories. Three very different lenses on the same question: who's actually in control of your factory right now?

The attackers? The agents? The policy makers? Or — and this is the optimistic read — the engineers who can finally use sensor data their plants have been generating for years and just didn't know what to do with?

Here's what caught our attention:

Foxconn Just Spent Eleven Days Running a Factory on Paper Timesheets

On May 1st at 7:00 AM, the Wi-Fi cut out at Foxconn's Mount Pleasant, Wisconsin facility. By 11 AM, the rest of the plant's network was gone too. Workers were told to power down their computers and not log back in "under any circumstances." Time-card terminals went dark. People filled out their hours on paper.

Eleven days later, Foxconn finally confirmed what its employees had already figured out: they'd been hit by ransomware.

The details:

The Nitrogen ransomware gang — a Conti 2 offshoot (the leaked codebase from the now-defunct Russian ransomware operation that's spawned a whole family of copycat groups since 2022) that's been active since 2023 — claimed responsibility on Monday, May 11th, posting Foxconn to its dark web leak site. The group says it walked away with 8 terabytes of data spanning over 11 million files, including project documentation and technical drawings tied to Apple, Intel, Google, Dell, Nvidia, and AMD.

Foxconn confirmed the breach to The Register on Tuesday, saying its cybersecurity team "activated the response mechanism" and that affected factories are "resuming normal production." The company declined to confirm whether any customer data was actually taken.

A few things worth noting:

- The Mount Pleasant facility primarily makes televisions and data servers, not iPhones — so Apple users can probably exhale. Sample files in the leak don't appear to contain Apple product specs.

- The bigger concern, according to security analyst Mark Henderson, is the network topology data for Google, Intel, and AMD that was reportedly stolen. Those are architectural maps of live data center infrastructure — useful intel for anyone planning their next attack.

- This isn't Foxconn's first ransomware rodeo. LockBit hit them in 2022 and 2024. DoppelPaymer demanded $34 million from a Mexican facility in 2020.

The bottom line:

The Foxconn attack isn't interesting because of the celebrity customer files. It's interesting because of how a corporate network compromise turned into a factory floor outage — and how routine that pattern has become. The fix isn't novel technology. It's segmentation, tested incident response, and accepting that your plant network isn't safe just because you can't ping it from Starbucks.

Read the full Register report →

SAP Wants to Run Your Business. Also, You Can't Bring Your Own AI.

Last week at SAP Sapphire in Orlando, CEO Christian Klein stood in front of 30,000 people and answered the question SAP has apparently been asking itself: "Will we be a software company in the future?"

The answer, delivered via the company's own AI assistant: "SAP is becoming a business AI company."

That's marketing speak. Here's what it actually means: SAP just launched 224 AI agents and 51 assistants designed to autonomously execute business processes across finance, supply chain, procurement, HR, and customer experience. The flashy keynote got the headlines. The quieter story — and arguably the more important one — is an updated API policy published in late April that says third-party AI agents can no longer make autonomous decisions over SAP data. If you want AI agents in your S/4HANA workflows, you go through Joule.

The details:

There are really two announcements to track, and they reinforce each other.

The agents. The new Autonomous Enterprise vision rests on three pillars: a unified Business AI Platform merging SAP BTP, Business Data Cloud, and Business AI; an Autonomous Suite with 200+ agents (including manufacturing-specific ones like the Production Excellence Agent and Production Master Data Readiness Agent); and Joule Studio for building custom agents. SAP cited Takeda achieving "up to 10% productivity gains" through what it's calling Autonomous Regulated Manufacturing. Anthropic's Claude is now a foundation model option. NVIDIA provides the secure runtime. AWS, Google Cloud, and Microsoft get bi-directional interoperability — eventually.

The API policy. In late April, SAP published API Policy v4/2026. Section 2.2.2 prohibits the use of SAP APIs for "interaction or integration with (semi-)autonomous or generative AI systems that plan, select, or execute sequences of API calls." Plain English: a non-SAP AI agent making autonomous decisions on S/4HANA data is now a policy violation. SAP's own Joule Agents sit on the permitted side of that line. Approved pathways are SAP-owned — Joule, Business Data Cloud, BTP, the Joule Agent Gateway, and Integration Suite. The Agent Gateway, notably, isn't even generally available yet.

The blowback was immediate. The DSAG (the German-speaking SAP user group, one of the most influential customer voices in the SAP ecosystem) formally demanded contractual clarity and protection for existing integrations. Klein told investors on the Q1 call that customers won't pay to access their own data and that SAP's architecture remains open. The written policy hasn't changed since he said so.

Why this matters:

Strip away the keynote production values and look at what's actually happening. SAP is building a perimeter around the data your business generates — the production orders, supplier records, financial transactions, and operational signals that you created using your own equipment, your own people, and your own processes — and declaring that the only sanctioned way to apply AI to that data is through SAP's infrastructure, running SAP's models (and SAP's partners' models), priced under SAP's consumption meter.

If that pattern sounds familiar, it should.

SAP has done this before. In 2017, customers were shocked to learn that connecting external systems to SAP without specific licenses could trigger massive "indirect access" claims. Diageo lost a UK court case and owed SAP £54 million because Salesforce users had indirectly accessed SAP data. SAP pursued AB InBev for a reported $600 million in a separate dispute that was eventually settled. The "Digital Access" model SAP introduced in 2018 was the compromise — and the receipt that this is how they negotiate.

Section 2.2.2 is the 2026 version of the same play, applied to AI agents. And the commercial logic is worth saying out loud: SAP doesn't just want you using Joule. SAP wants to be the broker that decides which AI gets access to your business data and at what price. Look at the partner list announced at Sapphire — Anthropic's Claude as a foundation model, NVIDIA providing the secure runtime via OpenShell, AWS providing zero-copy data integration to Amazon Athena. Those aren't customer relationships. Those are data flow relationships. The question every manufacturing customer should be asking is: when an external AI provider gets to reason over enterprise data through Joule's sanctioned pathway, what does SAP get in return for being the gatekeeper?

The answer is two-fold: AI Unit consumption (every agent interaction through Joule runs roughly €7 per unit, adding up fast at enterprise scale) and data gravity. The Master Data Readiness Agent, Business Data Cloud, and Knowledge Graph all do the same thing strategically — pull more of your operational data into SAP's governed environment, where the cost of moving it elsewhere goes up every year.

Three things to track if you run SAP on the manufacturing side.

1. Some of your existing integrations are probably in a gray area. If your team has connected Microsoft Copilot, Salesforce Einstein, or a custom pipeline to S/4HANA via OData APIs to execute business workflows autonomously, that's exactly what Section 2.2.2 targets. A Copilot helping a developer write ABAP (SAP's proprietary programming language for customizing the platform) is fine. An agent making autonomous decisions about production orders, supplier lead times, or inventory positions over public APIs is not. Worth a written audit before your next contract conversation.

2. The asymmetry is the point. SAP's own Joule Agents face no such restriction on the same data. So enterprises running third-party agent strategies now have a compliance problem that enterprises using Joule don't. DSAG's 2026 Investment Survey shows only 3% of SAP customers use Joule in production today, which is why SAP set up a €100M fund to push partner adoption. Policy v4/2026 is a much stronger forcing function than that fund.

3. The data is the product now. That Production Master Data Readiness Agent isn't a coincidence. SAP knows the dirty secret of manufacturing IT: master data quality is terrible. Material masters with missing lead times. BOMs untouched since 2017. Routings that describe a machine you decommissioned. SAP is offering to help you clean it up — and once it's clean, sitting in Business Data Cloud, governed by SAP, accessed by SAP's chosen AI partners. Convenient.

The bottom line:

The technology is real. The agents are real. The manufacturing use cases are genuinely interesting. But Section 2.2.2 is a commercial fence around customer data, executed by a vendor that has spent the last decade demonstrating exactly how it monetizes the gates it builds.

Klein told investors customers won't pay to access their own data. Technically true. SAP isn't charging you for your data. They're charging you for the AI middleware required to access it. The data stays free. The only sanctioned path to it doesn't.

Manufacturers who get serious about Sapphire's vision should get equally serious about reading the fine print — and remembering Diageo before the next renewal.

Read the SAP 2026 recap → | Independent analysis of Section 2.2.2 →

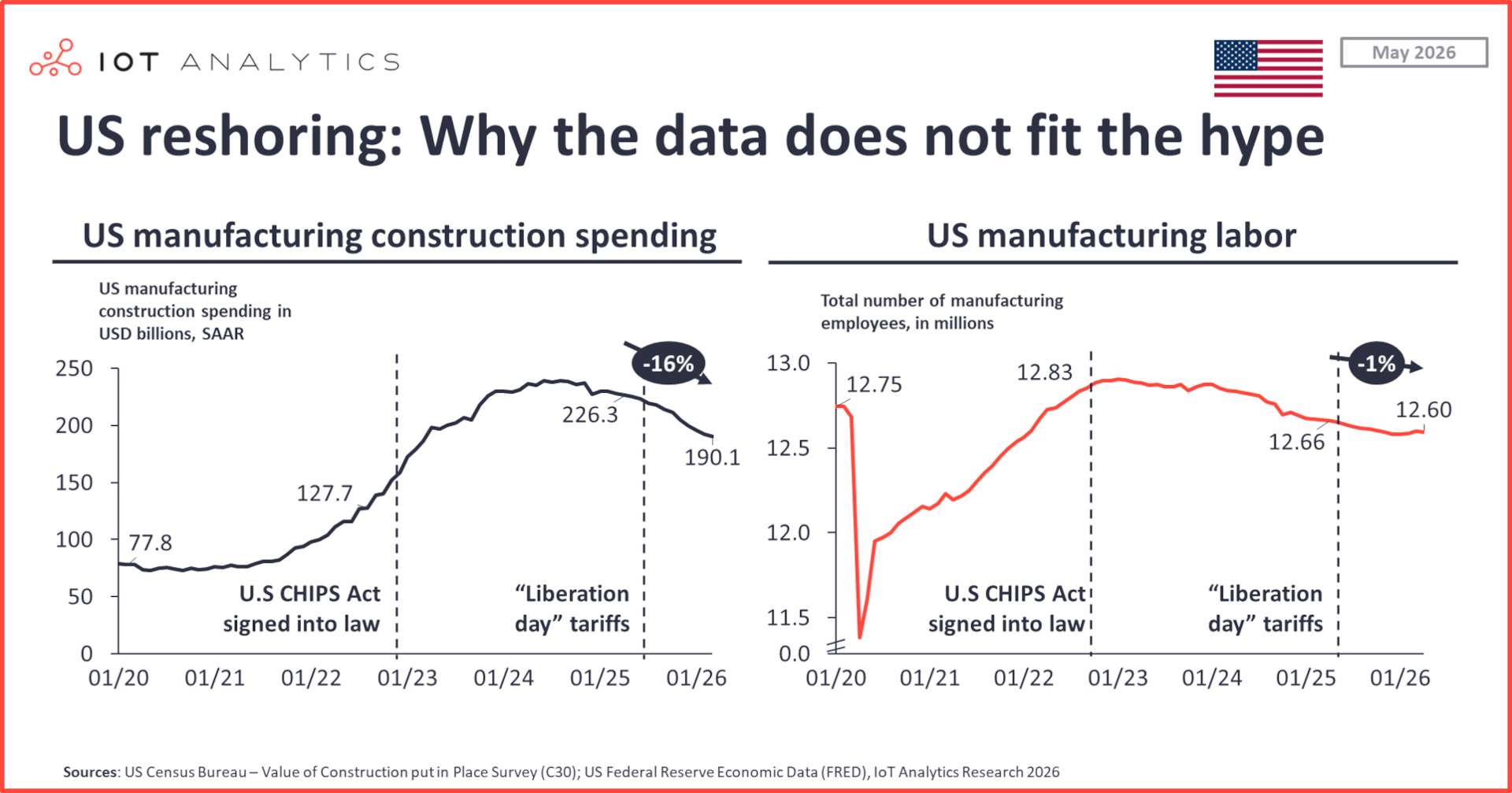

The Reshoring Boom That Isn't (According to the Data)

If you've been reading manufacturing trade press for the past year, you've heard some version of the same story: tariffs are driving the largest reshoring wave in American history, factories are roaring back, and trillions of dollars are flowing into domestic production.

The White House said it explicitly in an April 22nd press release: "the largest reshoring wave in American history as companies invest trillions to build and expand here at home."

Then, last Tuesday, IoT Analytics published its May 2026 Industrial Macro Pulse report and quietly reached a different conclusion: the reshoring boom, as far as the actual data shows, isn't happening.

The details:

A few numbers worth sitting with:

- US manufacturing construction spending has steadily declined since 2024, driven by a 44% slowdown in electronics factory and semiconductor fab construction since the mid-2024 peak. Strip out electronics, and construction spending has risen only 5.6% since the tariffs started — lower than you'd expect for a "boom."

- US manufacturing employment is down roughly 1% since the "Liberation Day" tariffs took effect, with only a slight uptick in February/March 2026.

- The Kearney Reshoring Index — which measures year-over-year change in the US manufacturing import ratio — was at -86 basis points for 2025, slightly less negative than 2024's -115, but still firmly in negative territory. Translation: the US imported more manufactured goods from low-cost Asian countries as a share of domestic output, not less.

- Kearney's own analysis of the data: despite US manufacturing investment announcements tripling over the past four years, domestic capacity has grown only 1.5%. Most projects are stuck in the announcement phase. Some have been abandoned.

The growth story IoT Analytics actually identified? Data centers and power infrastructure. S&P Global forecasts roughly $1.3 trillion in US energy utility capex between 2026 and 2030, driven primarily by data center demand. That's where the construction cranes are going — not new auto plants.

There's also the December ISM Supply Chain Planning Forecast, which found that 64% of manufacturers explicitly don't plan to reshore to avoid tariffs. Instead, 86% plan to pass cost increases on to customers in 2026.

Why this matters:

Three takeaways, and none of them are "panic."

1. Don't make capital decisions based on press releases. When a competitor announces a $500M domestic expansion, the data suggests there's a meaningful chance that project gets delayed, scaled back, or quietly abandoned in 18 months. Kearney's report found that announcement-to-completion ratios have gotten worse, not better. If your strategic plan assumes competitors are actually executing on their reshoring commitments at the announced pace, that's a bet — not a forecast.

2. The labor problem hasn't moved. Six months in, tariffs aren't fixing what the National Association of Manufacturers has been flagging for years: roughly 500,000 manufacturing jobs sit unfilled, and modern factories need digital, robotics, and AI skills that current training systems can't supply at scale. Tariffs change the cost equation; they don't change who can program a PLC or troubleshoot a vision system on second shift. Companies winning right now are the ones investing in automation and upskilling simultaneously.

3. The real demand wave is upstream of your factory. If you supply equipment, components, controls, or services to data centers and power generation, you're in the actual growth sector. AI-driven compute demand is forcing utility capex super-cycles, transformer and switchgear shortages, and grid infrastructure buildouts that will run for the rest of the decade. That's the construction spending data is actually pointing at.

The bottom line:

The reshoring story is louder than the data supports. Announcements aren't the same as construction, and construction isn't the same as production. The manufacturers making smart bets right now are the ones reading the macro carefully, investing in workforce capability, and paying close attention to where actual demand is forming — which, for now, is downstream of every AI training run in America.

Read the IoT Analytics report → | Kearney 2026 Reshoring Index →

Predictive Maintenance Finally Pencils Out — Even for Brownfield Plants

For the better part of a decade, predictive maintenance has been the technology everyone says they're going to deploy "next year." The pitch was good. The ROI math, less so. Sensors were expensive, integration was painful, and the AI models needed more clean data than most plants could produce.

That math has quietly changed. Per IBM and IDC analysis released earlier this year, AI-driven predictive maintenance has crossed an inflection point where the unit economics now work — not just at greenfield smart factories, but at brownfield plants retrofitting equipment built in the 1990s.

Here's what changed, and what it means for your maintenance budget.

The details:

The numbers driving this shift are big enough to matter:

- The predictive maintenance market is projected to grow from $10.93B in 2024 to over $70B by 2032 — a CAGR above 26%.

- Average manufacturing facility downtime now costs ~$260,000 per hour. For automotive, that figure hits $2.3 million per hour. Each hour of unplanned downtime is 50% more expensive than it was in 2019, driven by inflation, supply chain complexity, and tighter production schedules.

- A recently published General Motors case study found that after retrofitting legacy machines with IIoT sensors measuring vibration, temperature, pressure, humidity, and current draw, AI predicted 70%+ of equipment failures at least 24 hours in advance. Maintenance labor got redistributed toward genuinely at-risk equipment. Equipment life extended because over-maintenance dropped.

- McKinsey's broader research found predictive maintenance can reduce machine downtime by 20-40%. Less than a third of maintenance and operations teams have full or partial AI implementations today, but 65% plan to adopt within the next year.

- A 2026 academic case study using physics-informed AI models in a digital twin architecture showed 35% improvement in predictive accuracy, 40% reduction in unplanned downtime, and 25% optimization in maintenance costs compared to traditional approaches.

The technology stack that makes this work is no longer exotic. Vibration and temperature sensors are commodity items. Edge processing handles the latency-sensitive analysis locally. 5G and Wi-Fi 6 give you the bandwidth to ship time-series data to the cloud for model training. Generative AI is now being used to create synthetic failure datasets — useful when real failure data is rare (which it should be, in any well-run plant).

Why this matters for manufacturing:

The most important shift isn't the technology — it's that brownfield retrofits now have a credible ROI story.

For most of the last decade, predictive maintenance pilots ran on new equipment with embedded sensors. The "rip and replace" requirement made it a non-starter for plants running older machines with another 10-15 years of useful life. That's changed.

Three things worth knowing if you're sitting on a fleet of legacy equipment:

1. The sensor cost has collapsed. Industrial-grade vibration sensors that cost $500-1,500 a decade ago now run $50-200. A typical retrofit pilot — covering, say, 20 critical motors and pumps in a single production line — fits in a maintenance budget conversation rather than a capital project.

2. ROI windows have compressed to 12-18 months for mid-sized plants. That's based on published case study data, not vendor marketing. The driver isn't a single magic number — it's the combination of avoided downtime, reduced over-maintenance, and extended equipment life adding up faster than they used to.

3. The hardest part is still the data, not the AI. Models need labeled failure data to learn from. Most maintenance management systems (CMMS) are filled with free-text fault descriptions that vary by technician and shift. "Bearing noisy," "unusual vibration on east pump," and "#3 motor rough" might all describe the same failure mode — but to a machine learning model, they look like three different events. The plants getting predictive maintenance right are the ones investing in CMMS data cleanup before the AI deployment, not after.

Real-world scenario:

Your maintenance supervisor walks in Monday morning with the same conversation he's been having for three years: the #4 conveyor motor failed Saturday night, we lost six hours on Line 2, and the replacement bearings are on back-order from Germany.

Now imagine that same conversation three months from now, after a sensor retrofit on the top 20 critical assets. Instead, the supervisor says: "The vibration profile on the #4 motor started drifting Thursday afternoon. The model flagged it Friday morning. We swapped it during Sunday's planned downtime. No production impact."

That's a real before/after, and it's the operational reality companies like GM are now reporting publicly. The technology to do this isn't science fiction. It's commodity sensors, edge gateways, and a maintenance team that's been re-tooled to act on predictions instead of reacting to failures.

What it requires from you: a real data audit, a willingness to fix CMMS hygiene before the AI project starts, and pilot scoping that picks the right 15-20 assets — the ones where failure is expensive and the failure modes are detectable with the sensors you can afford.

The bottom line:

The predictive maintenance pitch finally matches the unit economics. The plants getting there first aren't the ones with the biggest IT budgets — they're the ones doing the unglamorous work of fixing maintenance data quality, picking the right starter assets, and treating sensors as a maintenance line item instead of a capital project. For most brownfield manufacturers, this is the highest-ROI Industry 4.0 investment available right now.

Read the predictive maintenance 2026 guide → | GM predictive maintenance case study →

Byte-Sized Brilliance

Here's a number that should make every manufacturing executive a little uncomfortable: of the AI projects manufacturers announced in 2025, fewer than one in five made it into actual production by the end of the year.

That's not a hit piece. That's Gartner's and McKinsey's own data on enterprise AI deployment, looking specifically at manufacturing. The rest are stuck in pilot purgatory — proofs of concept that proved the concept, then never escaped the lab.

For context, the average mid-sized manufacturing plant generates roughly 1 terabyte of operational data per day — temperature readings, vibration signatures, cycle times, quality measurements, line speeds, energy consumption. That's the equivalent of about 250,000 photos a day, every day, per plant. A modest 10-plant operation produces enough data annually to fill the entire US Library of Congress text collection — twice.

And yet, in 2026, we're still publishing case studies celebrating manufacturers who managed to use some of that data to predict some of their failures, some of the time.

The bottleneck was never the technology. SCADA systems have been logging this stuff since the 1990s. Historians have been compressing and storing it since the early 2000s. PLCs cost less than a decent laptop. The bottleneck is the gap between generating data, trusting it enough to act on it, and building the organizational muscle to actually do something with it on the plant floor.

Industry 4.0 was never going to be won by the company with the most sensors or the fanciest AI agents. It's going to be won by the company that finally figures out how to turn its own existing data into operational decisions — at scale, repeatedly, on a Tuesday at 3 AM when nobody important is watching.

That's not a technology problem. That's a discipline problem. And discipline, unlike compute, doesn't get cheaper every year.

Let us know how we're doing! https://forms.gle/zSXrKTK9BNZ3BrpXA

Responses